Advisors hear it all the time: Long-term care insurance is too expensive. Or, I have enough assets to cover my own expenses.

But a recent Wall Street Journal article paints a very different picture. One family spent $1.3 million over the past decade on home care for their elderly mother—an amount that few retirees anticipate needing. (WSJ article here.)

That’s the problem with long-term care: it’s unpredictable, expensive, and too often underestimated. Even clients who believe they can self-fund may not fully grasp the financial strain that prolonged care needs can place on an estate—especially if they want to leave a legacy for a spouse or children.

The Medicare Myth

Many clients assume Medicare will step in and cover long-term care expenses. Unfortunately, this is a costly misunderstanding. Medicare only pays for a maximum of 100 days of rehabilitation or skilled nursing care after a qualifying hospital stay. That’s it.

After that? The bill is theirs to pay—unless they’ve qualified for Medicaid, which requires spending down assets to near-poverty levels. For middle-class and affluent retirees, that’s not an option they want to consider, particularly when a surviving spouse may still need those assets for their own retirement.

After all, 70 percent of adults who survive to age 65 develop severe LTC needs before they die and 48 percent receive some paid care over their lifetime

The Stop-Gap Strategy: A Smarter Way to Self-Insure

Instead of hoping for the best or depleting assets, a more strategic approach is to create a long-term care stop-gap—a financial buffer that absorbs part or all of the care expenses while allowing the estate to continue growing.

And unlike self-funding, where tax deductions may be limited, every dollar from this LTC benefit is tax-free—making it even more efficient.

Here’s how it works:

- Take a portion of the estate’s liquid assets—for example, $100,000 from a $1,000,000 estate.

- Invest it into a specialized long-term care annuity that earns a non guaranteed 6%, with a small fee for the LTC rider.

- Instantly create $300,000 of long-term care coverage that pays benefits over six years.

- The cash value at the end of year one shows a net growth of 4.27%, preserving the original premium amount.

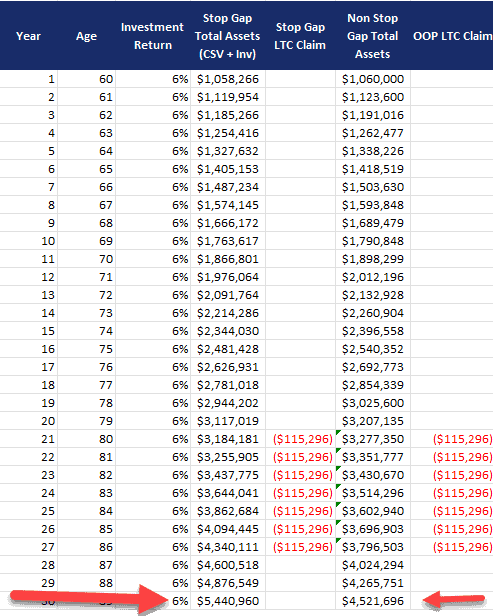

At first glance, this might not seem like a massive number compared to a potential $1.3 million LTC expense. But let’s look at the real impact on a 60 year old male client who puts $100,000 into the stopgap.

If the insured doesn’t need care, the annuity continues growing at around 4.27% (net after LTC rider charges)—preserving wealth rather than depleting it.

If the insured does go on claim at age 80, they now have:

- $9,608 tax-free per month available for long-term care expenses

- $807,802 total in long-term care benefits

- Coverage that absorbs nearly all of a $10,000/month LTC bill, significantly reducing the burden on the estate

What does this mean for the overall financial picture?

Even after funding years of care expenses, the estate still grows by nearly $1,000,000 over life expectancy compared to self-insuring. Instead of liquidating other investments or selling assets in a down market, this strategy lets the estate preserve wealth while efficiently covering care costs.

In both approaches, asset growth appears similar at first. But when a long-term care event occurs, the stop-gap strategy enables the estate to maintain and even grow in value, while the self-funded approach sees a significant depletion.

Why This Approach Works

Unlike traditional long-term care insurance, which requires ongoing premiums that could be lost if never used, this method keeps control in the client’s hands. The funds are still part of the estate, still earning, and still accessible—but now they also provide leverage against one of the biggest threats to retirement security.

For clients who balk at the cost of long-term care insurance, this approach reframes the conversation. It’s not about paying for insurance—it’s about shifting risk while keeping financial control.

The Bottom Line

Long-term care isn’t just a risk—it’s a near certainty for many retirees. And the cost isn’t just measured in dollars, but in the financial strain it places on families and the legacy they hoped to leave behind.

With a simple stop-gap strategy, clients can protect their assets, reduce their risk, and still grow their wealth—all while covering a major portion of their long-term care needs.

If you’d like to see the numbers in action, let’s walk through a spreadsheet example together. A small shift in planning can mean hundreds of thousands of dollars in preserved wealth.

Want to see how this could work for your clients? Let’s walk through real-world numbers together.